.png)

We at Ambit are constantly trying to stay ahead of the curve by drowning out the noise and looking ahead. In keeping with our long-term investment thesis, we like to stay up to date with not just the present impediments faced by your portfolio companies but also long-term disruptions which can hit these companies. Hence we will regularly come out with our thoughts on disruptions in your portfolio companies/ sectors and for the 22nd Volume of this series we have selected Mastek.

This note takes a closer look at (1) Mastek’s journey since its early days (2) the challenges it faced (3) Its current avatar (4) the possible disruptions that it may face over the longer run and how the company is placed to tackle those.

One of the oldest IT companies in India – Mastek was incorporated in 1982 as Management and Software Technology Pvt. Ltd by IIM students – Ashank Desai, R. Sundar and Ketan Mehta who were later joined by Sudhakar Ram. The company changed its name to Mastek in 1992, around the time of IPO which was also the year Majesco – Mastek’s Insurance products business – was founded. The founders did not want this to be another programming shop and intended on creating a business focused on designing and delivering computer software by “Synthesizing management principles and technology capabilities”. Its London Congestion Charging project (a system of charging a daily fee for driving through congested areas), along with Capita, has been instrumental in addressing traffic issues in London and is a testament to Mastek’s capabilities. Majesco was later demerged from the company in FY15 and listed in the USA on NYSE before its eventual divestment.

A Path less trodden – Unlike other IT services companies of the time, Mastek’s approach was unique – Products over services, domestic over exports, exporting to APAC before the US, onsite subsidiary model, to name a few. It had many industry firsts: (1) 1st IT company in India to offer ESOP as early as 1993, (2) The first IT company in the world to get People CMM (P-CMM Level-3) (3) 1st Indian product company to be listed on NYSE. This unique journey over the last 4 decades, however, has been marred with similarly unique challenges. Therefore, it is important to look at these unique elements in the company’s journey – in addition to the changes – for us to understand the company’s metamorphosis into its current avatar.

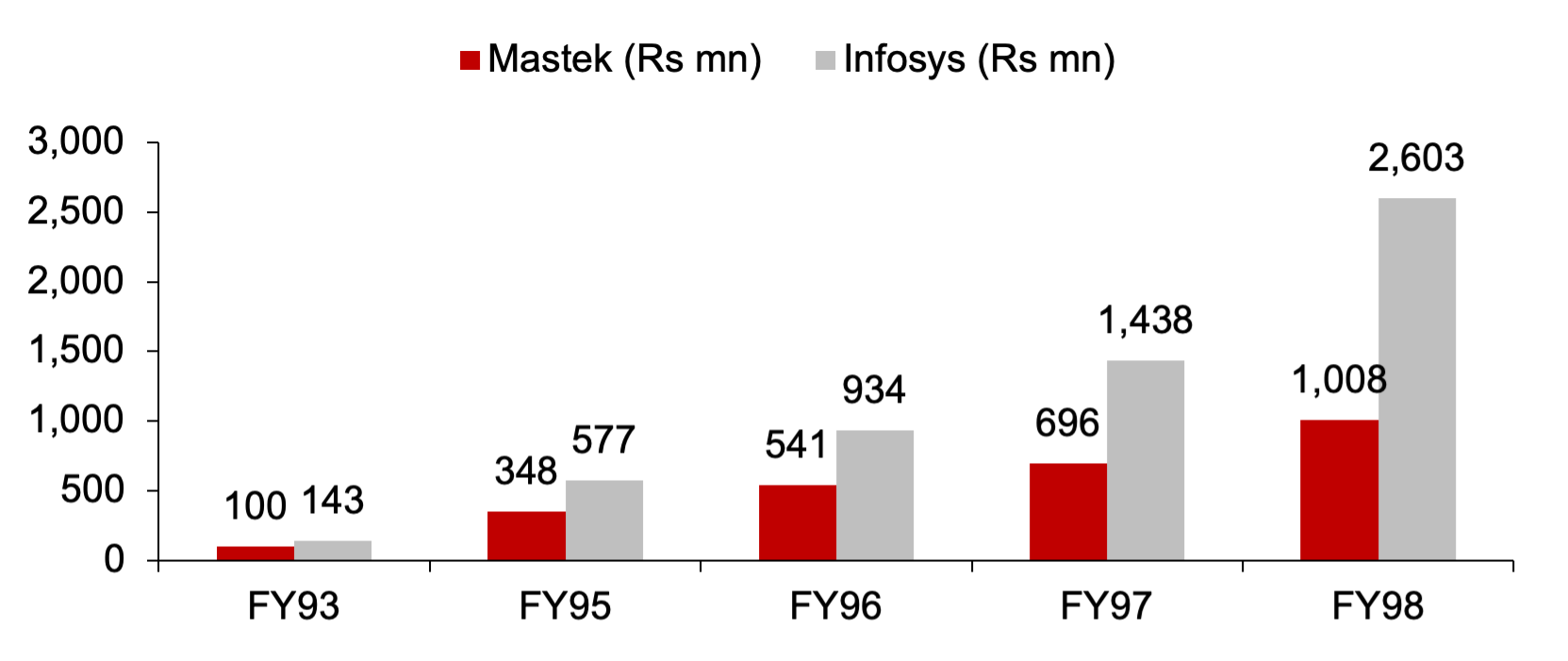

Exhibit 1: Mastek’s revenue at the time of its IPO was comparable with Infosys

Source: Ambit Asset Management, Company Annual Reports, Note: FY94 data not available for Mastek

Domestic first: Unlike peers, MAST took 10 years before venturing into exports, with ~80% of its revenue at the time of IPO coming from the domestic market. In exports too, it started from APAC countries rather than US. It bore the brunt of the Asian Financial Crisis in the late 90s when its clients – largely brokers and financiers – were the most impacted.

Product-led approach: One of the 1st companies in India to build software products. It had a mix of its own products – in manufacturing and stock broking segments – and distributed products. Product Development, however, involves high upfront costs with back-ended revenue and a high risk of failure. MAMIS, an ERP, faced tough competition from the likes of SAP and Oracle owing to interface and compatibility challenges, and thus could not succeed.

Missing the Y2K Bandwagon: Made a conscious call to stay away from Y2K work and instead chose to work on internet-based newer technologies and ‘IT Solutions’. This was in contrast to peers that followed a strategy of ‘size’. While these peers got a foot in the door of large enterprises and scaled up much faster, Mastek lost a fair bit of money when most of the internet-based companies went under post the dot-com bubble.

Subsidiary Model: In contrast to the conventional India-centric model, Mastek formed 100% subsidiary in geographies where it achieved decent scale. It organized them as an SBU led by a local management team with decision-making autonomy and a Development Centre in India. Benefits of higher accountability and better talent management were negated by higher investment, compliance/taxation and working capital, impacting short-term financials.

Mastek First – Defining Focus Areas: Post 2000, Mastek decided to narrow down on select focus areas. Under the ‘Mastek First’ initiative, it decided to focus on large customers, particularly in the Financial space where it was strong in the Insurance vertical, and in System Integration and large Projects – such as the London Congestion project.

Product or Services: Albeit delayed, Mastek eventually caught up in the Services segment with ~90% of revenues in the late 90s coming from services. While the decision to focus on certain core areas defined the company’s strength, it also limited its presence in some fast-growing but commoditized segments. Continued investment in product development ate in on the margins of the services business – which too was reeling with post-GFC headwinds and program deferrals in the UK. Hence, a decision was taken in FY15 to chart out separate trajectories for each of these businesses and demerge them.

The Mastek today –

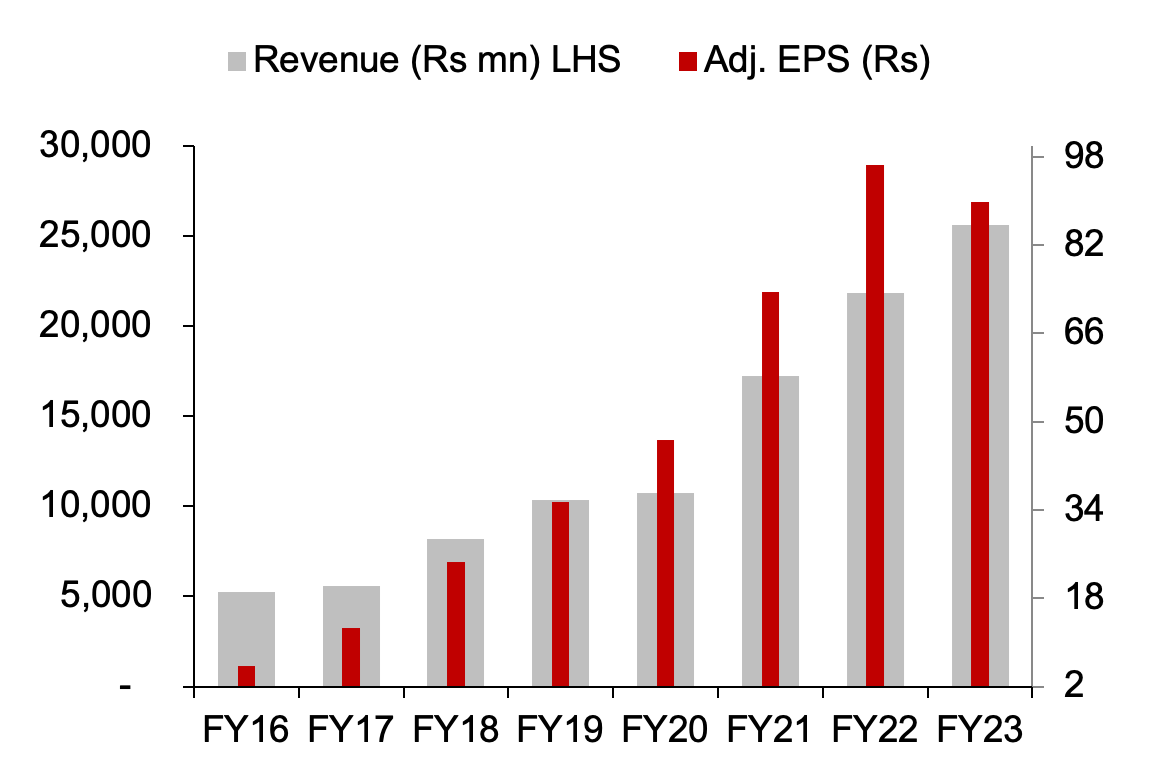

Post de-merger of Masjeco in FY15, MAST was predominantly UK focused with ~95% revenue from the geography where it was working with government agencies. Over the next 7 years, the company worked on (1) Adding presence in the largest growth market - the US (2) Expanding service areas (3) Professionalizing / institutionalizing the company. Its Revenue/EPS (incl. inorganic) has compounded at 25%/48% CAGR over the last 7 years.

Mastek today is an IT service company with a strong presence in the UK government business where it has evolved over the years from a subcontractor for large SIs such as BT or Capita – to participating in contracts directly. It is largely a Digital company with limited exposure to legacy services. Acquisitions of Evosys/MST Solutions have helped Mastek add to its offerings in Oracle/Salesforce and expanded its US presence to 24% of overall revenue. The company aspires to reach the $1bn revenue mark in the latter half of this decade – a 3x jump from its current $0.3bn annual run rate.

While from a numbers perspective, MAST may not have matched its peer from the IPO times – a comparison that often pops up – it is important to highlight and at the same time appreciate the different path the company undertook which has created a strong foundation for future growth. Its adherence to that philosophy over the years, strong corporate governance standards and employee-first approach will be instrumental in paving the way for the next leg of growth.

Exhibit 2: Mastek’s Revenue/EPS have grown @ 25%/48% CAGR since FY16…

Source: Ambit Asset Management, advice-cloud.co.uk

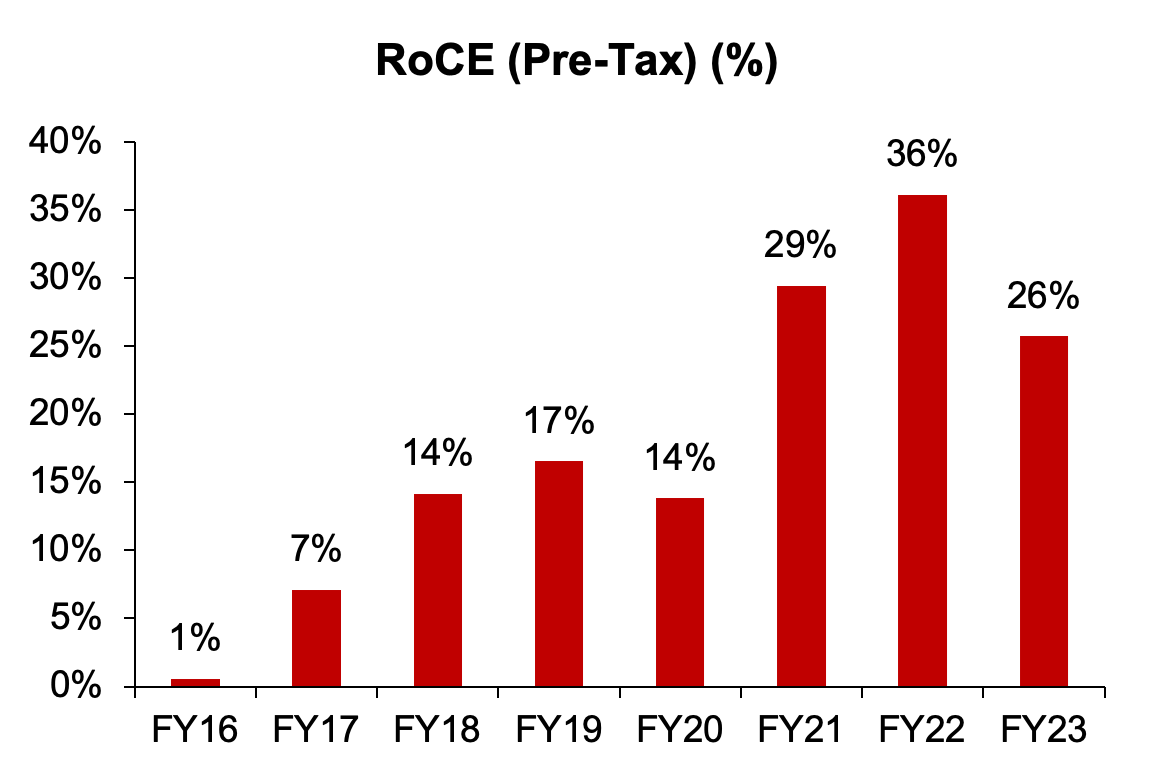

Exhibit 3: …with improving return ratios resulting in 40% price CAGR

Source: Ambit Asset Management, advice-cloud.co.uk

Scanning for Disruptions –

- The UK government business – The successful execution of the London Congestion Charging project was a defining moment in Mastek’s journey. It created good visibility and enabled them to expand their footprint in the Public sector vertical in the UK. It helped secure a deal with BT for NHS and further strengthened its relationship with Capita. Since then, the company has established itself as a capable partner and worked has worked closely with various Government departments in the UK such as NHS, Home Office, Border Agency, etc. thus creating a strong niche for itself. While these departments may address different end-user segments, there is a common set of underlying capabilities involved, such as working with multiple vendors and managing complex large-scale programs. Currently, UK constitutes the lion’s share of ~55-60% of revenue from Government vertical.

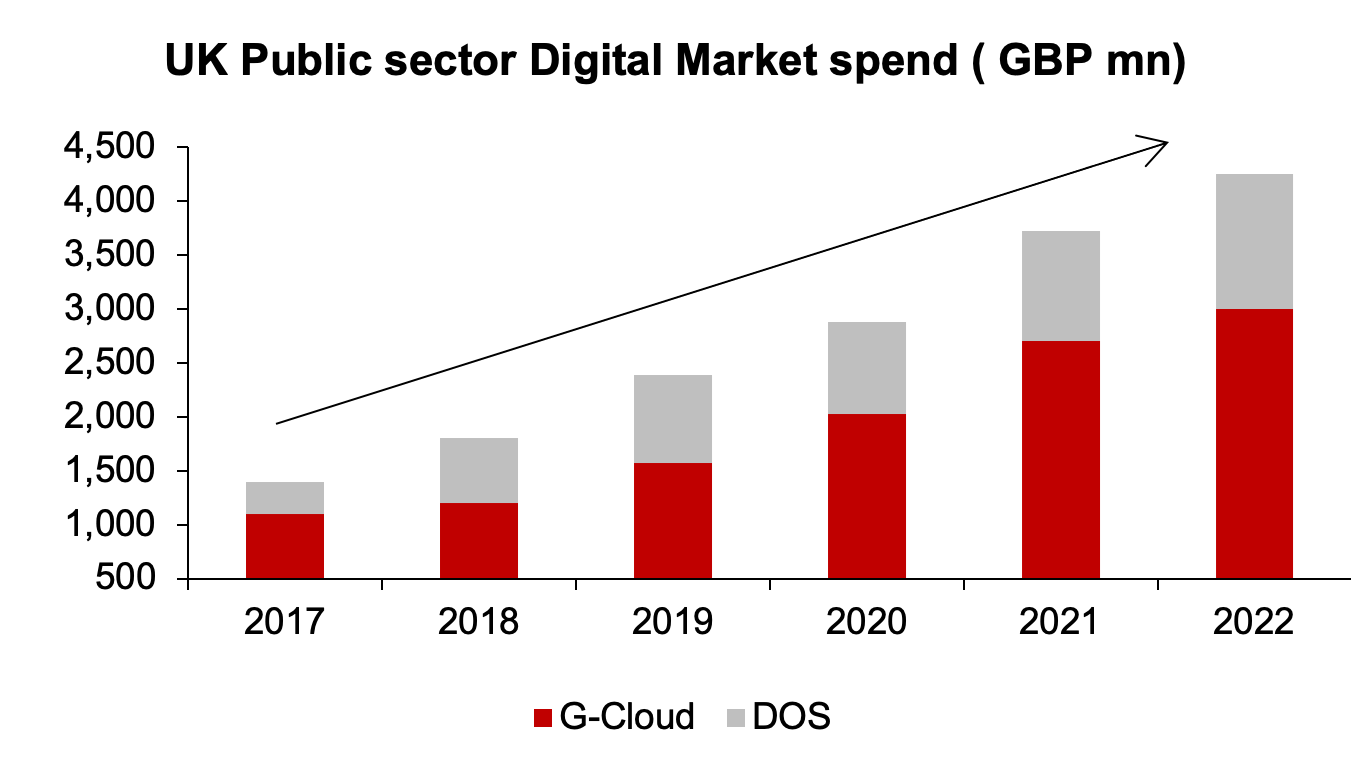

- Understanding the UK Public Sector Market: In the UK, public sector entities can procure various Digital IT services through a Government Digital Marketplace online platform which was created in 2014. Public sector digital spends in this marketplace via two key frameworks – DOS and GCloud – stand at ~GBP4.2bn (25% 5yr CAGR) (Refer Exhibit: 4). Thus, contrary to common perception, it is a fast-growing market with good margins and on-time payments. Before the Digital Marketplace was created in 2014, the procurement system involved a lengthy and complex tender process and the contracts here were usually large (~$1bn range) and mostly given to large European System Integrators (SIs) who then outsourced some component to companies such as Mastek. However, there were major slip-ups by some of these large SIs which resulted in administrative headaches and multiple protests which called for an overhaul. The Digital Marketplace was created for Public Sector for buying any IT commodity or services. The government also made it a level playing field by encouraging participation from the widest range of suppliers. This saw companies like Mastek participate directly in the deals.

Exhibit 4: Despite macro headwinds UK public sector Digital spends have grown at 25% CAGR over the last 5 yrsExhibit 4: Despite macro headwinds UK public sector Digital spends have grown at 25% CAGR over the last 5 yrs

Source: Ambit Asset Management, advice-cloud.co.uk

Exhibit 5: Mastek was ranked 5th/11th supplier in DOS/GCloud framework in 2021

Source: Ambit Asset Management, advice-cloud.co.uk

- The Challenges: As with any government business, the UK Public sector is also fraught with its own challenges –

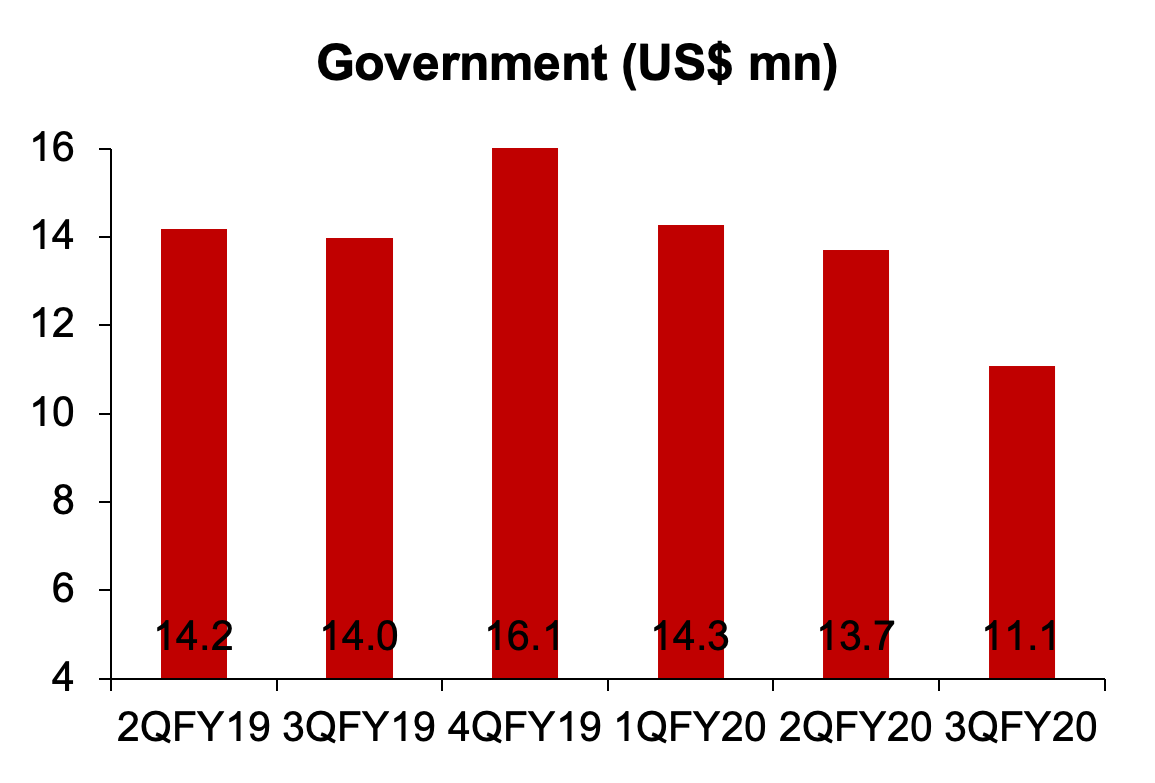

- Political instability and decision-making paralysis: Mastek faced a sharp decline in FY10 owing to the ramp-down of large project development in the BT/NHS program following GFC. Similarly, Brexit deadline pushback and UK re-elections impacted growth in 2019-20. Last year in 2022, an NHS internal restructuring and the ensuing decision-making paralysis saw a freeze on all new programs impacting Mastek (Refer Exhibit: 6&7).

- Change of framework: The Digital Marketplace framework replaced an earlier system called Government Procurement Services where the tender process was lengthy, complex and larger in size with limited opportunity/participation from SMEs. Recently, a new portal – Public Procurement Gateway (PPG) – was set up by the Government to replace the Digital Marketplace sighting challenges with the earlier technology and inability to accommodate growing customer demand. This new platform however is fraught with its own challenges of limited transparency, inferior user experience and difficulty in SME participation. While the newer framework may not impact Mastek materially (it may in fact prove beneficial), a risk of any such future overhaul or change in procurement that leads to extended uncertainty may pose a challenge to Mastek.

- Limited replication of projects/use cases: Unlike enterprise projects, government projects are often unique and may have limited opportunities for replication for enterprise clients. However, MAST at its end is creating case-study from these projects and pitching various use cases to commercial clients.

Exhibit 6: Decline in govt revenue owing to decision paralysis following re-election and Brexit led uncertainty

Source: Ambit Asset Management, Company Note: Old segmental classification

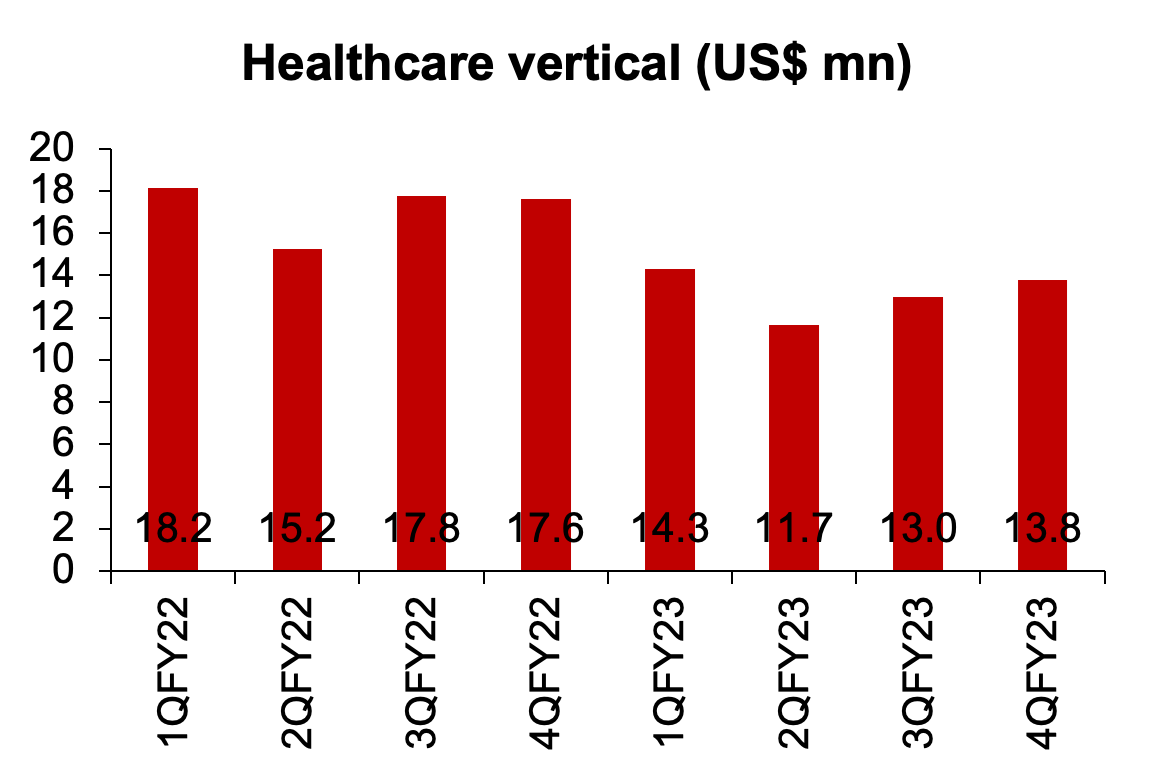

Exhibit 7: Similarly FY23 witnessed a decline due to the deferment of a program from the NHS

Source: Ambit Asset Management, Company Note: Most but not all Health vertical revenue pertains to govt

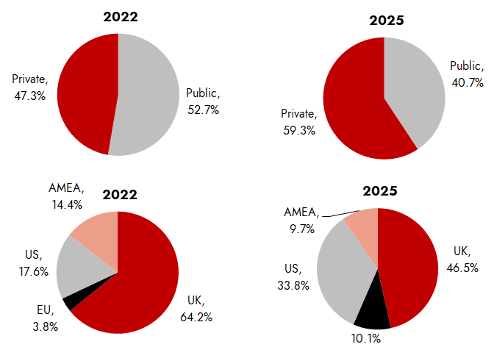

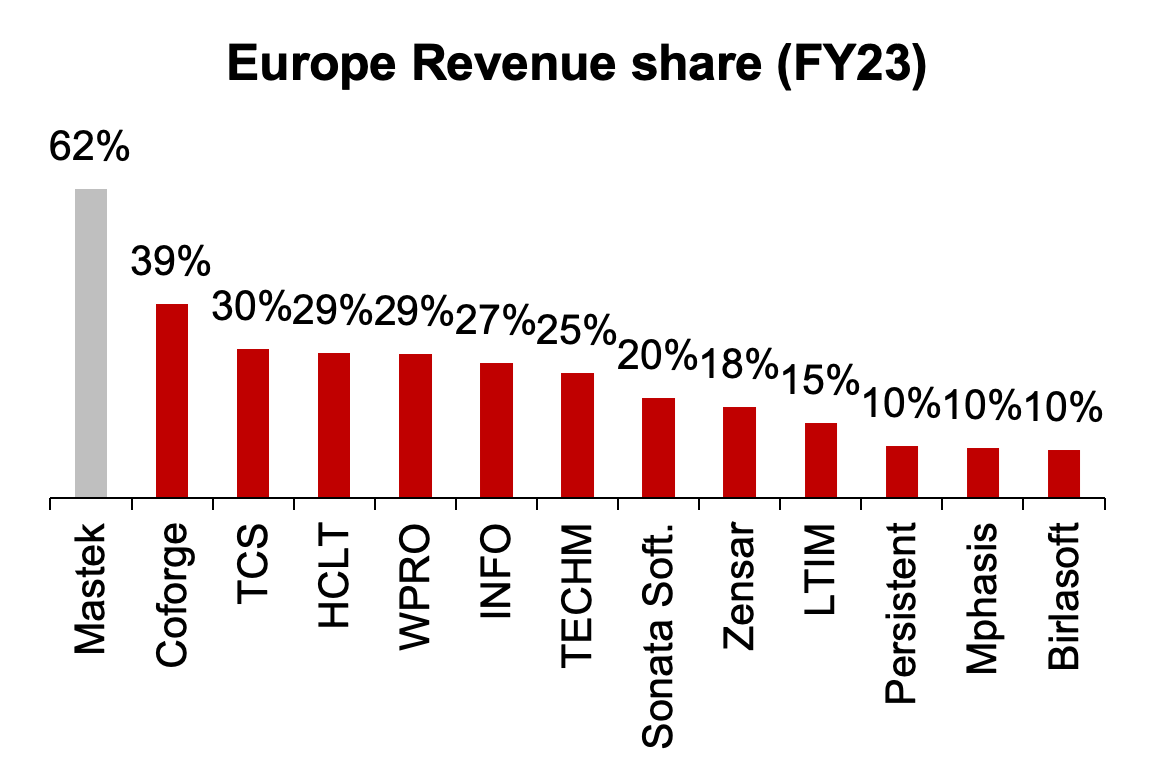

Mastek intends to reduce its dependence on the Government and bring down its overall Public sector revenue share from ~53% in FY22 to ~40% by FY25 (Refer Exhibit: 8). However, it will still be a meaningful share and one of the highest among Indian IT (to the geography and vertical) (Refer Exhibit: 9). Any structural challenge, especially in the UK government body could impact the company materially and increase near-term volatility.

On the flip side, while acknowledging the innate volatility in the UK government business, it is important to note that the business is sticky with high entry barriers. There is limited or no offshoring allowed – at least in the initial period – due to the sensitive nature of the work and data involved. Mastek has created strong in-roads in terms of relationship and execution track record in a market with a huge TAM – which largely offsets the revenue volatility risks. It will be important to see if MAST can replicate similar successful execution in other areas and diversify the revenue profile of the company.

Exhibit 8: MAST plans to reduce concentration substantially by 2025, however, it’ll still be higher than most peers

Source: Ambit Asset Management, MAST FY22 Investor Day Presentation

Exhibit 9: MAST’s current EU exposure is ~55% - much higher than that closest peer

Source: Ambit Asset Management, Company

2. Widening Service offerings –

A. How do IT Services companies engage with Hyperscalers / SaaS companies – In the complete Cloud Migration journey of a client, IT services companies partner with hyperscalers / SaaS companies (cloud providers) such as Amazon Web Services (AWS), Microsoft Azure, Google Cloud Oracle, Salesforce, etc to help their clients migrate to the Cloud. The IT services companies also provide additional tools & services for managing that infrastructure and building applications on the Cloud to help their clients extract maximum value. They often use a joint Go-To-Market (GTM) and enter into partnerships with the Cloud provider wherein the latter recommends the IT vendor to the enterprise looking to move to their public Cloud. It may also be in the form of a bundled package. The partners are chosen very carefully by the Cloud providers with various layers of certification and tiers involved as these partners would be quasi-representative of the cloud provider.

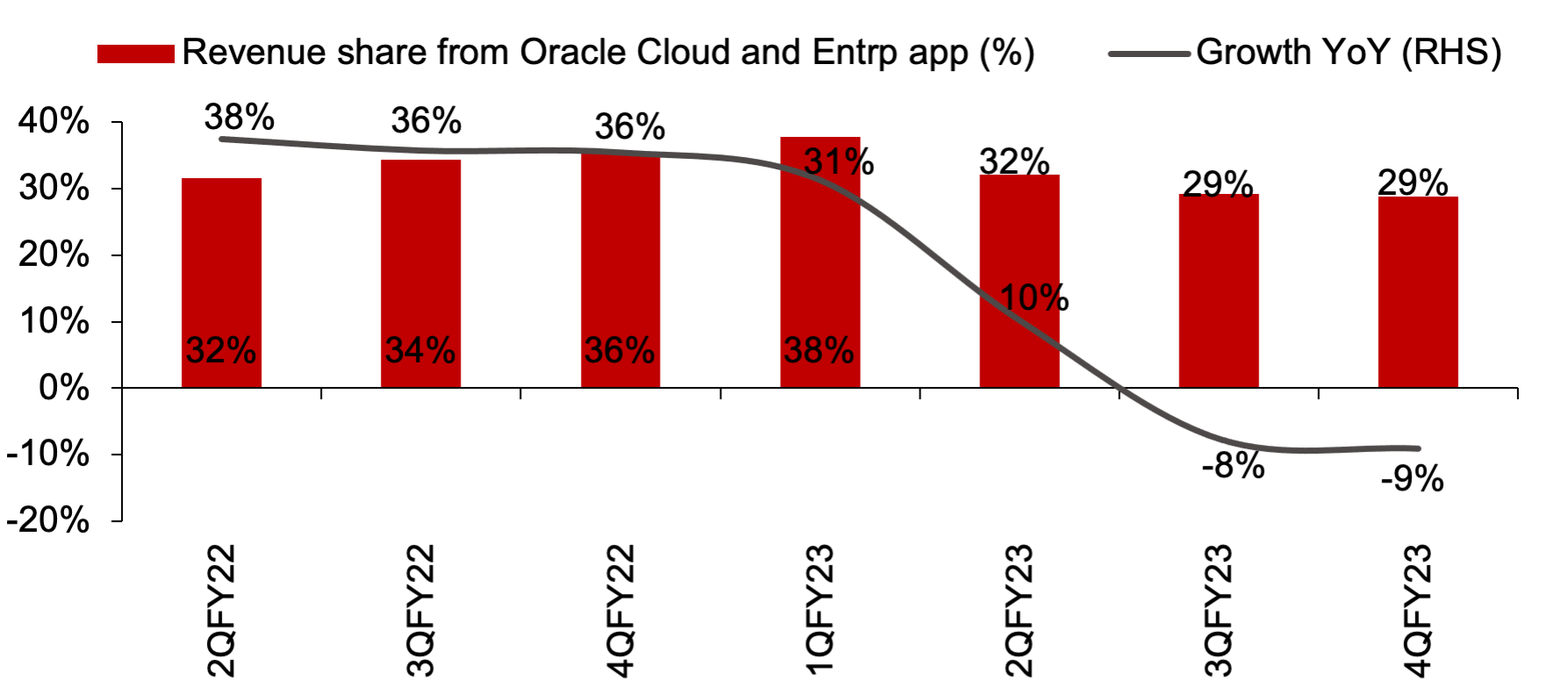

B. Mastek’s portfolio and current service offerings: Mastek’s current service offerings are strong in Oracle as well as Salesforce domain which combined constitute ~45-50% of overall revenue for the company. Going ahead, we feel that Mastek would need to widen its service offerings and expand its portfolio beyond Oracle and Salesforce and add other hyperscaler practices to participate in the complete digital transformation journey of the client. Focus on building partnerships and adding capabilities will further help diversify and de-risk revenue (Refer Exhibit: 10). Persistent is a good case-in-point where the company has expanded its offering across various hyperscaler over the last 24 months mainly via inorganic acquisitions and that is starting to play out. Mastek has identified certain key areas of growth where one of the focus areas will be growing AWS / Azure practice, which would be key to monitor.

Exhibit 10: Mastek’s Oracle revenue declined in H2FY23 as Oracle withdrew sales support for its Cloud Commerce component

Source: Ambit Asset Management, Company

3. Limited presence in the largest market – The USA –

Post the de-merger of Majesco in FY15, Mastek’s IT Services business was predominantly UK based with ~95% of revenues coming from that geography with no presence in the US, which is the largest addressable market resulting in missing significant growth opportunities. Since then Mastek has made three inorganic acquisitions in an attempt to enter and expand its US footprint:

-

- TAIS Tech in FY17: TAIS Tech specialized in implementation and support for Oracle Commerce (ATG & Endeca) and Oracle Commerce Cloud (OCC). It added ~$35m to MAST’s revenues in FY17 taking its US share from almost 0 to ~30%.

- Evosys in FY20: Evosys was a platinum partner for Oracle ERP (GL, payables, SCM, HCM). Although Evosys had a larger non-US presence relatively, it added ~$10mn or 30% to Mastek’s FY20 US revenue run rate. Through Evosys, MAST gained capabilities in BFSI and Hospitality in the US.

- MST Solutions in FY23: Meta Soft Tech Solutions (MST Solutions) is an independent Salesforce consulting partner.

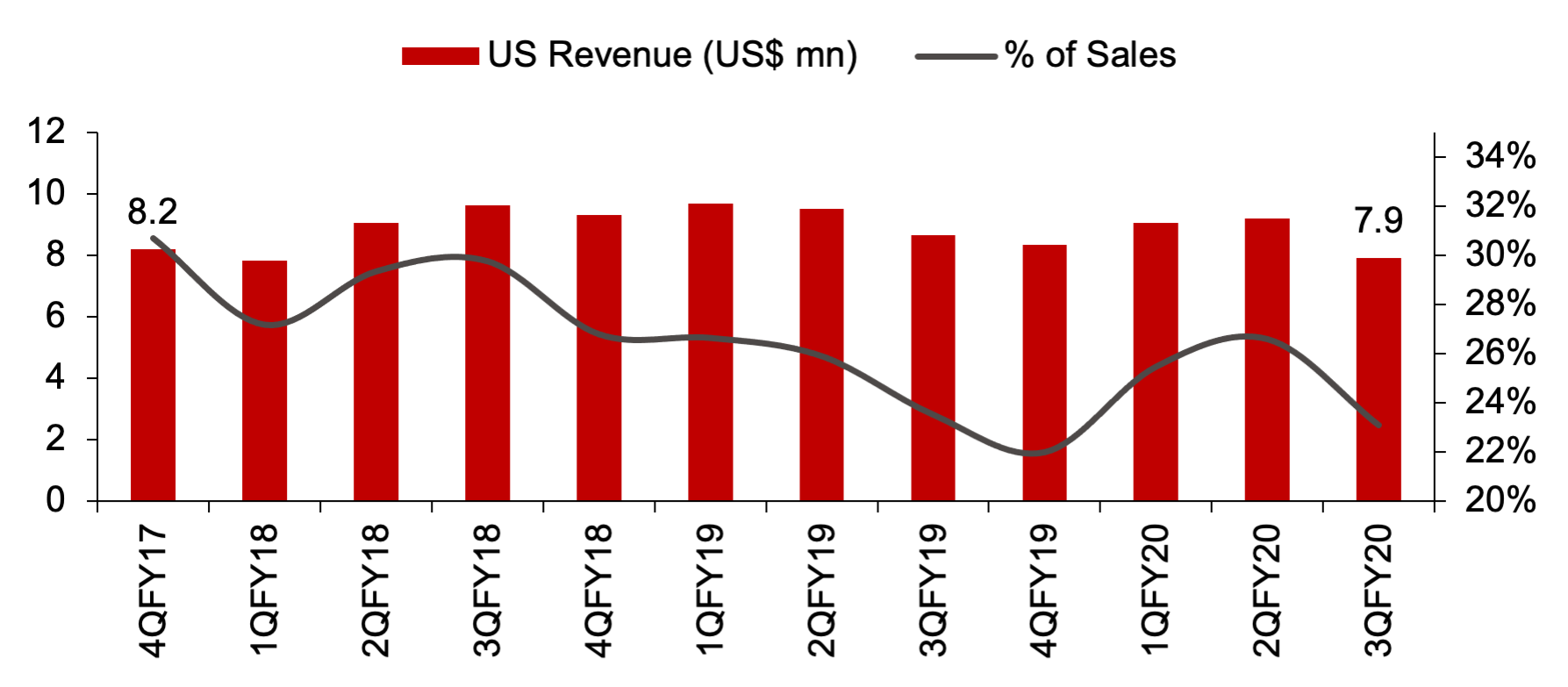

While MST Solutions is still young in the Mastek Group, TAIS Tech faced challenges post-acquisition when Oracle de-prioritized (in 2018) and subsequently withdrew sales support (2022) for its ATG / Oracle Cloud Commerce. This, along with headwinds in client-mining, has limited the organic growth in the US for Mastek. The current share from this geography is 24% which is the same as in FY19, before Evosys and MST acquisition (Refer Exhibit: 11). The company intends to derive 1/3rd of revenue out of the US by FY25 which will depend a lot on the leadership and execution in that geography. We did see signs of this in Q4FY23. If MAST can replicate its UK execution in the US over the medium to long term then that would lead to incremental re-rating for the company.

Exhibit 11: Mastek’s US revenue remained flat for 3 years owing to challenges in Oracle and limited client up / cross-sell

Source: Ambit Asset Management, Company

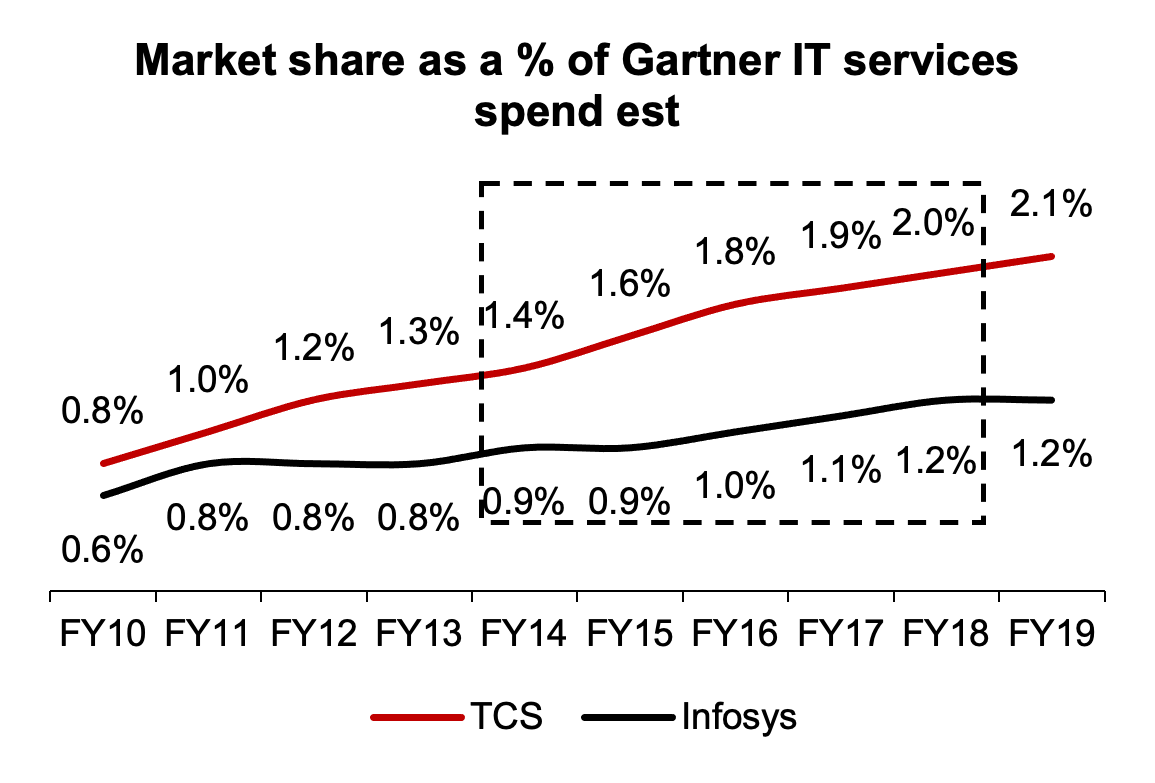

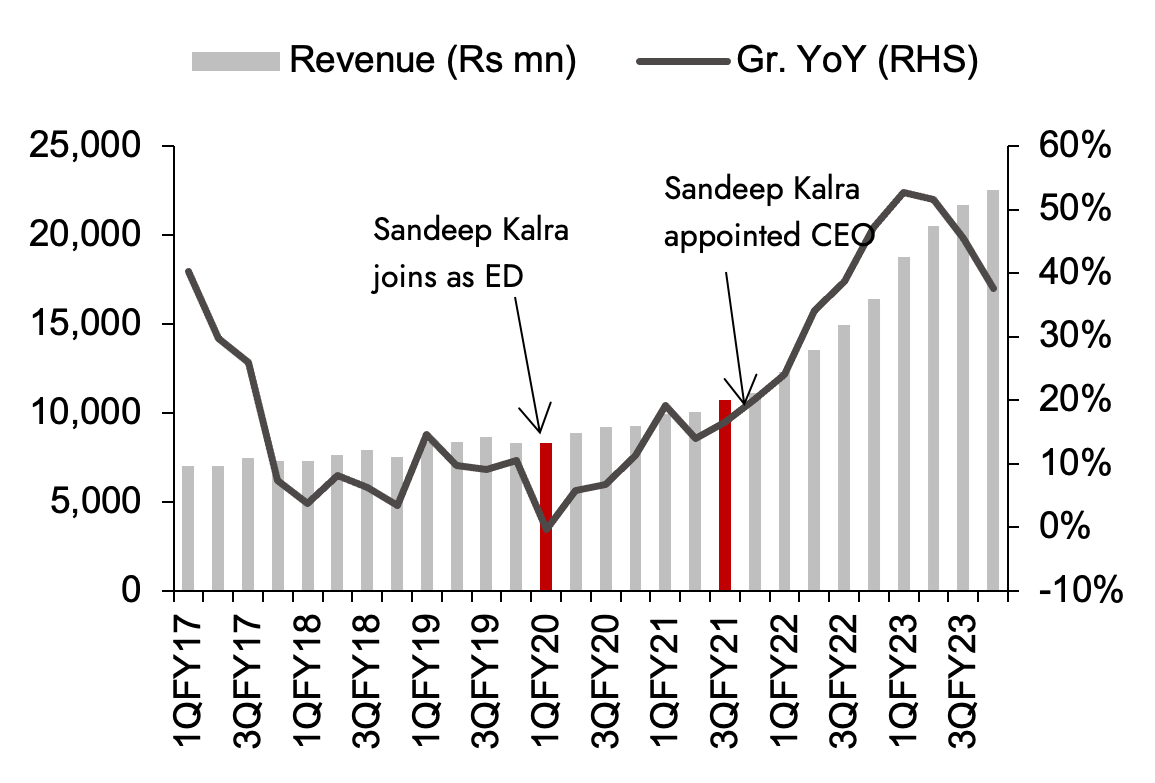

4. Successful institutionalization of the company: The transition to professional management is a crucial step in any company’s evolution. The idea is to de-risk from key-man risk, institutionalize processes and plan for the next leg of growth – once the company crosses a particular scale – by building best industry practices. Often, this journey is marred by headwinds and unplanned resistance resulting in instability and growth challenges for the company. Infosys, for eg, took its own time to adjust to this transition during which it lost market share to TCS (Refer exhibit: 12). Many other Indian IT companies have gone through similar phases in the past. However, once successfully executed, it can propel the company to the next orbit of growth as was seen in the case of Persistent (Refer Exhibit: 13).

Exhibit 12: Market-share gap between TCS and Infosys widened during the leadership transition/uncertainty

Source: Ambit Asset Management, Company Note: Market share is calculated as % of IT services spends as per Gartner estimates

Exhibit 13: PSYS’ performance has been the best among Tier1 and 2 since Sandeep Kalra took over

Source: Ambit Asset Management, Company

Mastek, for the longest time, was run by the promoters with the first outside CEO appointed only in 2016 when John Owens took over as the group CEO. He eventually relinquished the role in 2021 owing to challenges in relocating to the US. Mastek’s strategy required a focus on growing the US geography which called for the CEO to relocate. He was succeeded by Mr. Hiral Chandrana – the current CEO – who is based out of the USA and is working on building the US business. Mastek has also hired key top leaders over the last 12-15 months further strengthening its key leadership team (Refer Exhibit: 14). As Mastek transitions to a professional management set-up, any major top leadership churn or vision misalignment between the promoters and the management could set the company behind in its journey. We saw examples of this in other mid-tier companies which have been a key drag to their performance.

Exhibit 14: Some of the key hiring over the last one year

|

Name |

Designation |

Joined |

Prior Experience |

|

Ritwik Batabyal |

CTO & Innovaiton Officer |

Jan-22 |

Wipro, LTTS, Infosys |

|

Prajakta Talvelkar |

Global Head of Marketing & Partnerships |

Jan-22 |

Capgemini, Bristelcone |

|

Prameela Kalive |

COO |

Jan-23 |

Zensar |

|

Vijay Iyer |

President, Americas |

Mar-23 |

Persistent Systems, HCL Tech |

Source: Ambit Asset Management, Company

5. Foreign currency fluctuation – The majority of Indian IT exports have been to the US – a structurally strong economy – and in USD – the global reserve currency – thus acting as a tailwind for exporters. However, if the currency movement trend is reversed and the currency of the importing country weakens structurally over the longer term, it impacts the exporter negatively (Refer Exhibit: 15,16). To protect against near-term currency movements, companies hedge their forex exposure which eventually protects the net earnings impact, but the operating margins tend to get impacted in the near term. In Mastek’s case, we see the following implications of forex fluctuations –

- Exporting to a country with a structurally weakening currency: Mastek would continue to derive a large share of the revenue from the UK. Should the macroeconomic woes in the UK continue and the GBP structurally weakens, it will act as a major headwind to Mastek’s reported earnings.

- Exporting in a de-dollarized world: Talks around de-dollarization have risen over the last few years, especially after the Russia-Ukraine conflict. We covered this in detail in our May-23 newsletter. It would be very premature to comment on its impact – whether positive or negative – on Indian exporters. However, an event of that magnitude in the key import destination’s currency may create long-term ripples.

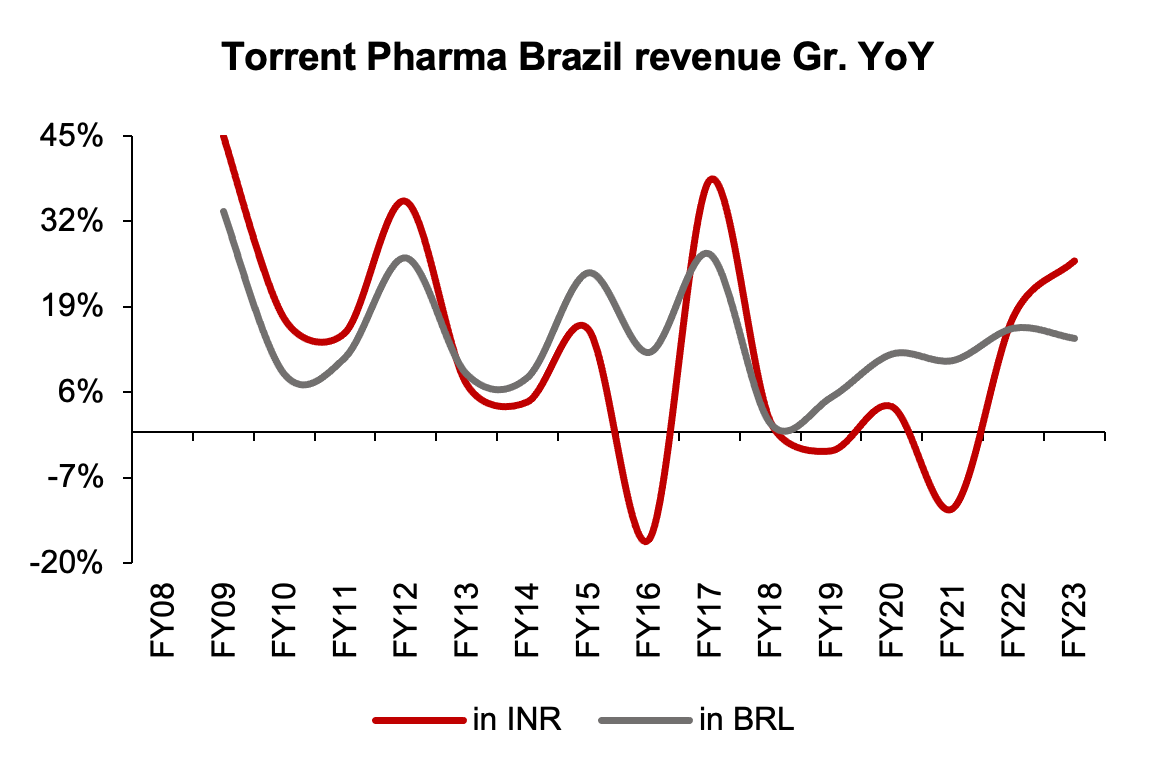

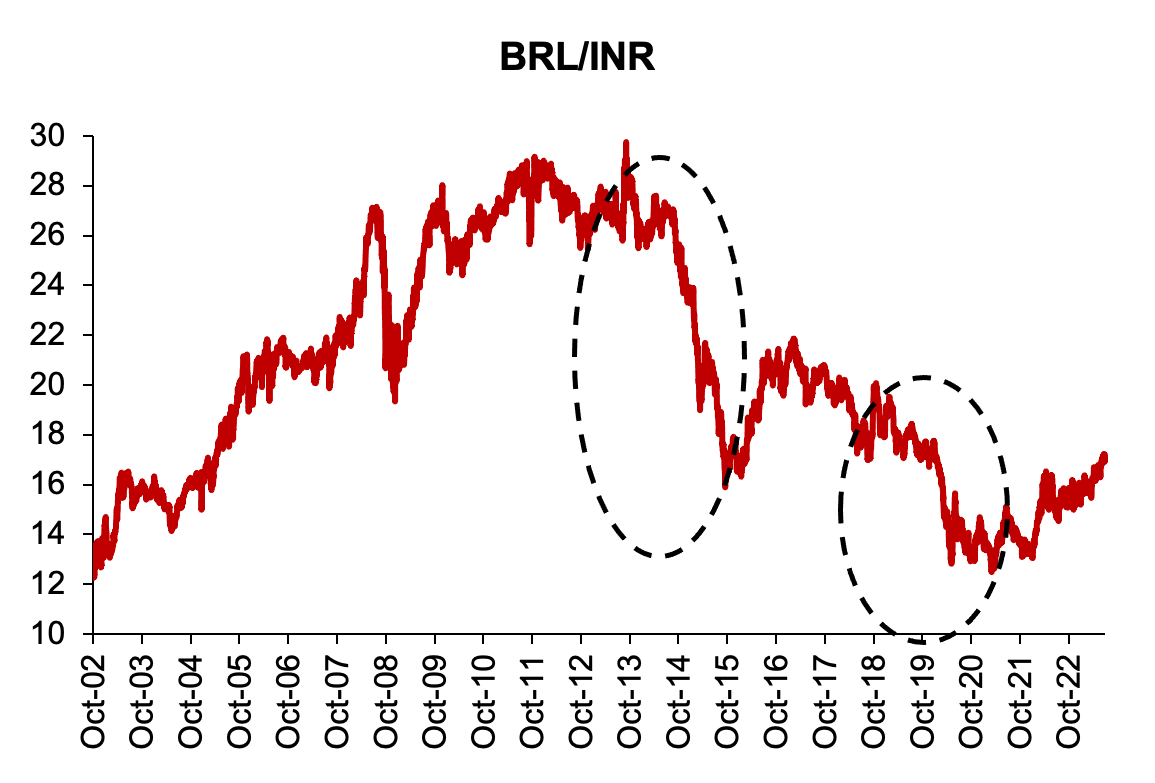

Exhibit 15: Difference between TRP’s local currency (BRL) and INR growth rate widened since FY15…

Source: Ambit Asset Management, Company

Exhibit 16: …owing to the structural reversal in currency movement implying ~6%* lower reported (INR) growth

Source: Ambit Asset Management, Bloomberg Note: CAGR from FY15-23 of TRP Brazil revenue in INR terms was 5.6% vs 12% in BRL

6. Generative AI – Traditional AI (Artificial Intelligence) use case is to identify patterns within specific data fed into the system to spell out recommendations. Generative AI, on the other hand, uses machine learning algorithms to create new content which did not exist earlier – whether it is chat response (Chat GPT) or image (Dall-E). While Generative AI has a rich history of over 5 years, the introduction of ChatGPT proved to be an ‘iPhone-like’ moment for the industry in terms of quality.

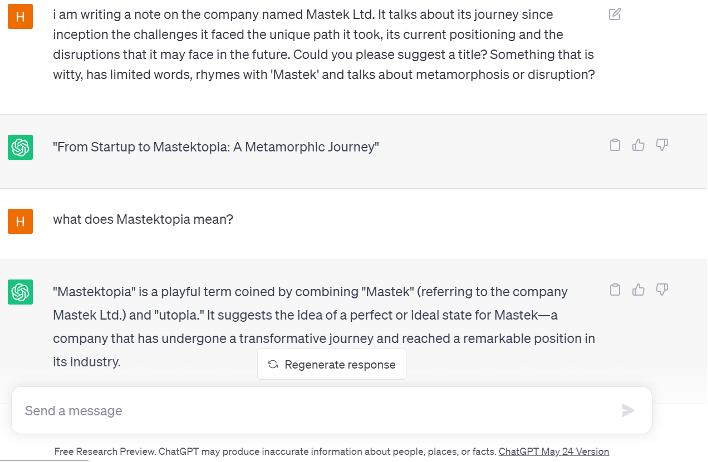

Exhibit 17: We asked ChatGPT to suggest a title for this report

Source: Ambit Asset Management, OpenAI (ChatGPT)

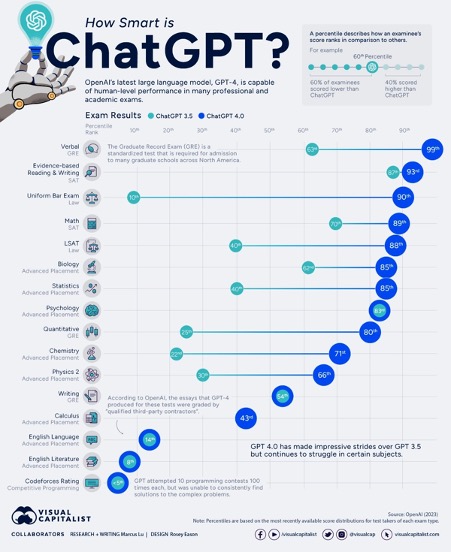

A. What will be its implications on the overall jobs market, especially Tech jobs?: Apart from basic learning and information-based use-cases, Generative AI can also perform technical functions such as writing code for software, summarizing financial statements of a company, diagnosing medical conditions, or even the title for this report (Refer Exhibit: 17). While these exceptional use cases facilitate better productivity, they have a flip side to it. As per a research paper by OpenAI – the creator of ChatGPT – ~80% of the U.S. workforce could have at least 10% of their work tasks affected by the introduction of GPTs, while around 19% of workers may see at least 50% of their tasks impacted.

Exhibit 18: ChatGPT (GPT4) would outscore most humans in various examinations

Source: Ambit Asset Management, Visual Capitalist

B. Impact on IT Services companies: While better developer productivity will lead to cost savings for IT vendors, it may negatively impact volumes, especially in a model where the client is billed for the Time & Effort spent on the project. While it is difficult to quantify the actual effect of lower volumes, it will vary across service lines and offerings depending on the type of work involved and the subsequent automation possibility.

- Segments such as BPO or Customer Support (L1 or touchpoints) will be more prone to disruption where Chatbots can take over easily. Chatbots usage – which we all find on major websites but struggle with engaging with the same – will take a major leap and user engagement will increase

- In terms of software development/programming, easier tasks such as creating a small website will be more vulnerable compared to enterprise-class applications – where instead of writing a 100-line code, the resource would have to monitor the code generated by GPT and suggest changes.

Industry estimates suggest ~11% overall impact on the global IT services spending pool (Refer Exhibit: 19,20). This will be higher for BPO and Application Development spending while relatively lower for Consulting and IMS

C. Implications for Mastek: While the impact will be much higher for Tier-2/3 companies, it will also be an opportunity to grab market share. Cost savings by enterprise clients could lead to deployment in other tech areas around Cloud and Cloud native technologies, thus fastening the digital upgradation cycle. It is important to note that Mastek has very limited legacy services baggage and NIL BPO exposure.

It would still be too early to spell out the final impact especially a doomsday scenario for tech developers and IT services companies. Agile movers will be able to differentiate themselves from the more rigid-structured larger players. IT services as a sector has been prone to disruption since the beginning and Indian IT companies have successfully reimagined and reinvented themselves during those period. They have leveraged each of the tech cycle change to offer value to clients and remain relevant throughout. Moreover, it is important to point out that companies that have started experimenting with Gen AI are facing several challenges in scale-up, security, data privacy and building viable use cases.

Conclusion

Mastek’s founders were visionary, tech enthusiasts with high corporate governance standards. But they were much ahead of their time. This had its benefits as well as drawbacks. After having navigated through multiple disruptions over the last 40 years, we feel the company is at an inflection point where successful execution can propel it to the next tier. Management aspires to reach the $1bn milestone in the latter half of the decade. In that, successful execution in the US market will be the key to watch out for.